23 May 2026

Mapping API Pathways: How ACH Networks and Credit Card Systems Converge in Mobile Environments to Uphold Compliance Standards

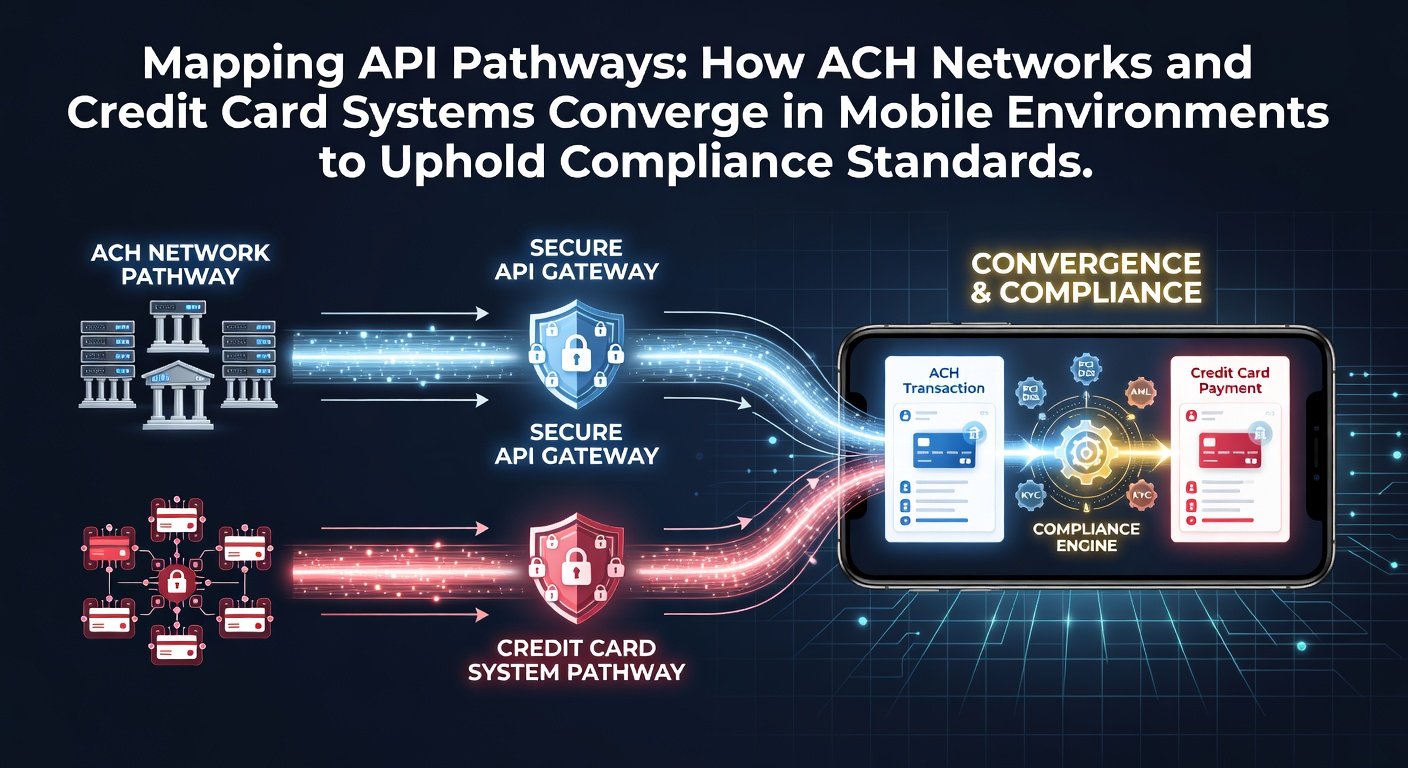

Payment pathways in mobile environments rely on application programming interfaces that connect ACH networks with credit card systems, and developers map these routes to maintain regulatory alignment across multiple jurisdictions. Mobile applications initiate transactions that route either through card rails for immediate authorization or ACH batches for direct bank debits, with APIs serving as the translation layer that enforces data formatting rules required by both networks.

Core Components of Network Integration

ACH transfers operate under rules set by NACHA and involve batch processing that typically settles within one to two business days, while credit card transactions follow real-time authorization protocols governed by card networks and PCI DSS requirements. APIs bridge these differences by standardizing message formats so that a single mobile interface can trigger either method without violating formatting mandates. Researchers at institutions tracking payment infrastructure note that such convergence reduces duplicate compliance checks because the same customer verification data feeds into both pathways when structured correctly.

API Design for Mobile Transaction Routing

Mobile developers implement layered API calls that first validate device-level security tokens, then query backend services to determine the optimal route based on transaction amount, merchant category, and user bank linkage status. When an ACH route activates, the API converts card-derived account details into NACHA-formatted files while preserving encryption standards that satisfy PCI requirements even though the funds never touch card networks. Credit card routes instead forward tokenized card data to processors, and the same compliance engine logs both outcomes for audit trails. Observers note that this dual-path architecture appears in production environments where transaction volume exceeds several million monthly events.

Compliance Mechanisms Across Converged Systems

Regulatory frameworks such as those outlined by the Federal Reserve require that any API handling ACH origination must embed OFAC screening and maintain records for at least six years. Card systems add EMVCo and PCI DSS layers that mandate point-to-point encryption during mobile transmission. When pathways converge, the API must satisfy the stricter control set at each junction; for instance, an ACH return code must map to an equivalent card decline reason code so downstream fraud systems receive consistent signals. Data published by the European Central Bank in its 2025 oversight reports shows that cross-rail reconciliation features lowered mismatch errors by measurable percentages in participating member states.

Developments Anticipated for May 2026

Industry documentation indicates that updated NACHA operating rules scheduled for May 2026 will require faster notification of unauthorized ACH debits through API webhooks, aligning response windows more closely with card network dispute timelines. Mobile application teams preparing for this change test unified notification endpoints that push alerts to both ACH originators and card issuers from a single event stream. Compliance teams also review how these webhook payloads must incorporate new data fields for same-day settlement programs already expanding in several districts. Such synchronization keeps mobile platforms from maintaining separate code branches for each network while meeting the forthcoming deadlines.

Real-World Implementation Patterns

One documented deployment involves a subscription service that routes monthly charges through ACH when users link verified bank accounts and switches to card rails for one-time add-on purchases. The governing API evaluates account age, previous return rates, and device fingerprint scores before selecting the route, thereby satisfying both NACHA risk management guidelines and card network velocity rules. Another example appears in gig-economy platforms that issue instant payouts via card push when drivers request same-day funds, yet default to ACH for weekly batch settlements to control interchange costs. Both patterns demonstrate that mapping logic embedded in APIs can enforce policy without exposing routing decisions to end users.

Security and Data Handling Practices

Encryption protocols remain consistent across routes even though settlement mechanics differ. Mobile SDKs tokenize sensitive elements at the device level before any API transmission occurs, and backend services decrypt only within PCI-compliant zones. Audit logs capture every route decision along with the compliance rule that triggered it, allowing examiners from bodies such as the Australian Securities and Investments Commission to reconstruct sequences during reviews. Organizations that maintain separate ACH and card gateways often discover redundant security modules, whereas converged API designs consolidate those modules into fewer touchpoints that undergo unified penetration testing cycles.

Conclusion

API pathways that link ACH networks with credit card systems in mobile settings deliver coordinated compliance by standardizing data flows, security controls, and reporting outputs. As May 2026 approaches, organizations that have already aligned their routing logic with forthcoming rule changes position themselves to meet updated notification and reconciliation requirements without architectural overhauls. The convergence continues to evolve through iterative updates to message schemas and risk engines rather than wholesale replacement of either network.