2 Jun 2026

Charting ACH Pathways in Mobile Merchant Ecosystems for PCI-Compliant Recurring Invoicing

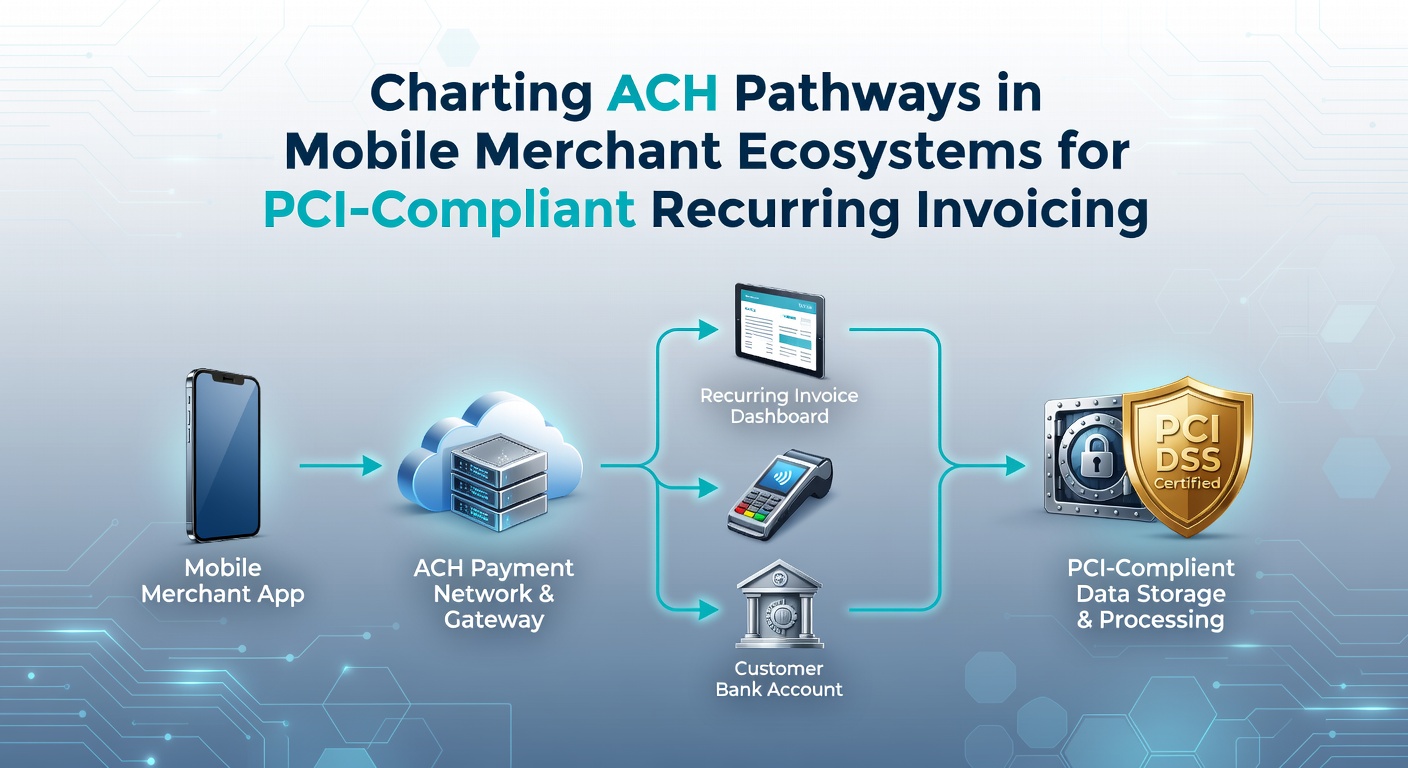

ACH pathways have become central to mobile merchant ecosystems because they enable direct bank transfers that support recurring invoicing without relying solely on card networks. These systems route funds through the Automated Clearing House network while meeting PCI DSS requirements that govern how payment data moves and gets stored. Observers note that businesses handling subscriptions often combine mobile apps with ACH to reduce processing costs and maintain compliance across repeated billing cycles.

Core Elements of ACH Integration in Mobile Environments

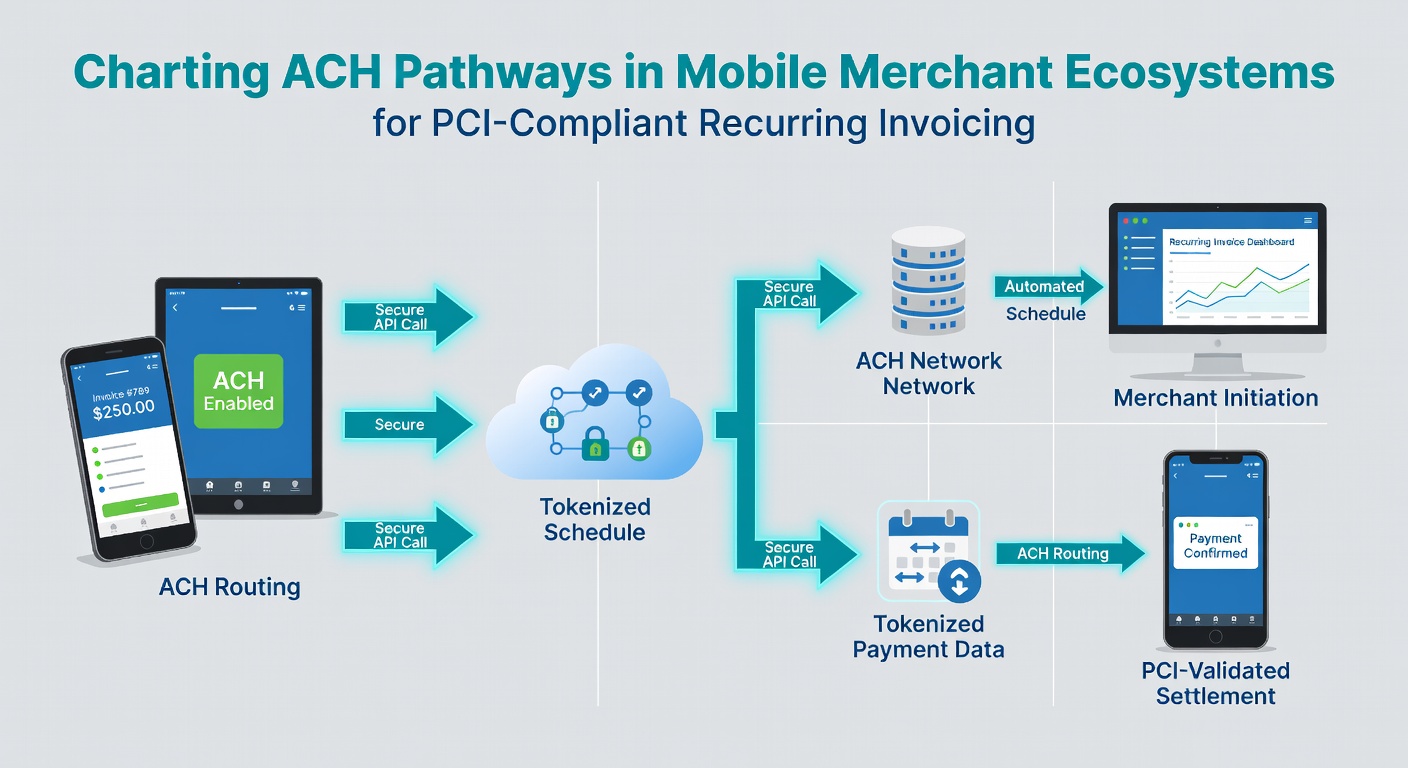

Mobile applications connect to ACH processors through secure APIs that tokenize bank account details rather than storing raw routing and account numbers on devices. This approach aligns with PCI standards because ACH transactions typically bypass cardholder data environments altogether. Data from industry reports indicates that merchants using these pathways process recurring invoices by initiating electronic debits on scheduled dates while the mobile interface handles user authentication through device biometrics and multi-factor prompts.

Developers map these connections by embedding SDKs that route authorization requests to ACH operators. The process begins when a customer enters bank credentials in the app, which then generates a secure token for future debits. Experts have observed that this tokenization layer keeps sensitive information off the merchant's servers, satisfying key PCI requirements around data minimization. As of mid-2026, ongoing updates to mobile operating systems continue to emphasize secure enclave storage for such tokens, which further supports compliance during recurring cycles.

Compliance Requirements for Recurring ACH Invoicing

PCI DSS mandates specific controls when payment data travels through mobile channels, even though ACH itself falls outside many card-specific rules. Merchants must still protect any card data collected during hybrid setups and maintain audit trails for all recurring authorizations. Research indicates that organizations achieve this by logging each ACH initiation separately from any card elements, creating distinct records that auditors can review without exposing full transaction histories.

Authorization forms presented in mobile apps require explicit customer consent for each recurring schedule, and systems automatically send notifications before debits occur. Those who've implemented these flows report that the combination of written mandates and digital confirmations satisfies both NACHA operating rules and PCI expectations around evidence of consent. PCI Security Standards Council guidelines outline how recurring transactions should segment data flows to limit exposure.

Technical Pathways Connecting Mobile Apps to ACH Networks

Integration typically occurs through gateways that translate mobile session data into NACHA-formatted files for batch processing. The pathway begins at the app layer, moves through an encrypted channel to the processor, and lands in the ACH operator's settlement queue. Studies have shown that real-time verification of account ownership during onboarding reduces return rates on subsequent recurring invoices.

Security protocols include end-to-end encryption during transmission and regular vulnerability scans on the mobile endpoints. Merchants also implement role-based access controls so only authorized personnel can adjust recurring schedules. Evidence suggests these layered defenses align with broader industry efforts to secure payment ecosystems as mobile usage grows.

Security Protocols and Risk Mitigation Practices

Token replacement for bank details serves as the primary defense against data breaches in recurring setups. When a token expires or a customer revokes authorization, the system immediately stops future debits without needing to handle raw account information. Observers have noted that this method keeps merchant systems outside the scope of certain PCI assessments because they never retain the original credentials.

Monitoring tools track unusual patterns in ACH returns, such as repeated NSF entries, and trigger reviews before the next cycle runs. European Central Bank analyses of payment security highlight how similar monitoring reduces operational risks in cross-border recurring flows. Merchants integrate these alerts directly into their mobile dashboards so finance teams can act quickly.

Future Developments in Mobile ACH Ecosystems

Standards bodies continue refining rules around instant ACH variants and their compatibility with PCI frameworks. Mobile platforms are incorporating deeper support for secure payment elements that streamline authorization while preserving compliance boundaries. Researchers continue to examine how these evolutions affect merchant adoption rates and settlement times across recurring invoice models.

Conclusion

ACH pathways in mobile merchant systems provide a structured route for PCI-compliant recurring invoicing by emphasizing tokenization, explicit consent mechanisms, and segmented data handling. The technical connections between apps and settlement networks rely on established encryption and logging practices that satisfy regulatory expectations. As these ecosystems mature, the focus remains on maintaining clear separation between sensitive credentials and merchant operations while supporting reliable payment cycles.